As per the OECD Economic Outlook, May 2024, India will be the fastest growing emerging economy amongst G20 nations. Economic growth in India is expected to be at 6.6% in 2024 and 2025 outperforming its major competitors in BRICS economies, Indonesia and Türkiye among others. This optimism has also been reflected in the provisional estimates (PE) released by the National Statistical Office (NSO), MOSPI, GoI on May 31, 2024, where the real Gross Domestic Product (GDP) is predicted to grow by 8.2% on y-o-y basis (in 2022-23, the growth rate is estimated to be at 7.0%) while the Gross Value Added (GVA) is predicted to grow by 7.2% in 2023-24 over the previous period’s growth rate of 6.7%

However, major components from demand and supply side growth exhibit a declining trend in the annual data. The supply side GDP growth measured in terms of Gross Value Added (GVA) is expected to show signs of recovery in the secondary sector led by the manufacturing and construction sector. While primary and tertiary sectors are expected to decline where significant declining trends emerge in the agriculture and services sector. The GDP from the expenditure side comprises consumption, investment, government spending and net exports which are also known as four engines or drivers of growth. The growth in investment i.e. Gross Fixed Capital Formation (GFCF) is estimated to grow from 6.62% in 2022-23 to 8.98% in 2023-24 as a result of continuous thrust on capital and infrastructure expenditure by the government. Nevertheless, other components of demand side GDP are projected to decline in 2023-24. Both the government expenditure (GFCE) and exports are estimated to decline significantly from 9.00% and 13.39% in 2022-23 to 2.45% and 2.63% in 2023-24 respectively. Similarly, there has been no respite on the burgeoning imports in 2023-24 as it registered more than proportionate growth vis-à-vis the exports. Failure to contain rising imports may prove detrimental to the overall balance of payments situation in the absence of adequate capital inflows.

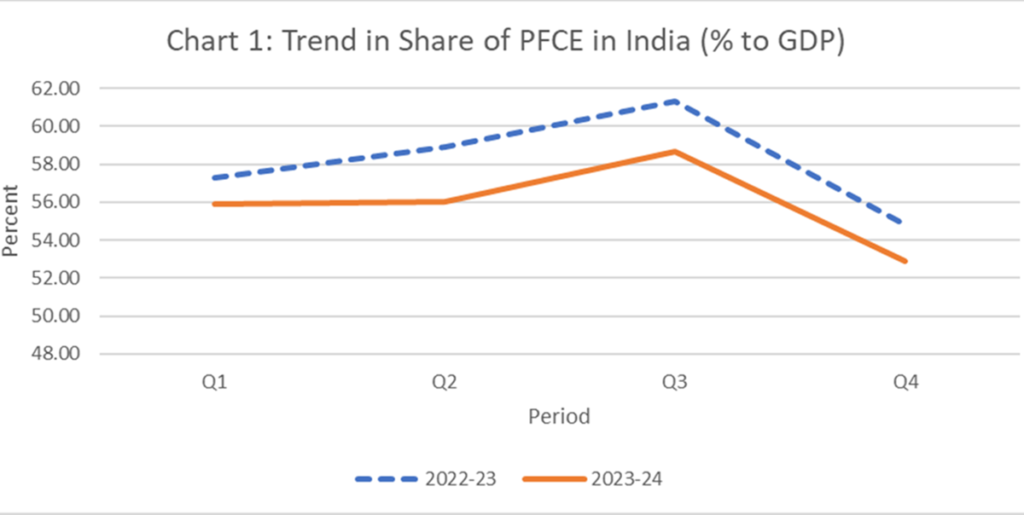

It is also important to note that during the previous year, higher growth level co-existed with the elevated level of inflationary pressures in the economy. The persistence of inflationary pressures has been reflected in the dwindling private consumption demand. The private final consumption expenditure (PFCE) is expected to decline from 6.77% in 2022-23 to 4.02% in 2023-24 on an annual basis as per the PE. Notably, there has been a continuous decline in the share of PFCE in the overall GDP from 58.1% in 2021-22 to 58.0% in 2022-23 and 55.8% in 2023-24. The continuous fall in the share of private consumption in the GDP is visible not only in the yearly growth trend but also in the trend of quarterly growth on a y-o-y basis (See Chart 1). Tepid growth in the PFCE along with a continuous decline in the share of PFCE in rising GDP indicate fall in the consumer expenditure on goods and services in the economy as a result of persistent and sticky inflation.

Apart from that, the imported inflation in terms of sudden rise in international crude oil prices and volatility in the food prices pose credible threats to the headline inflation in India. As per the headline inflation data released by the MOSPI, GoI on June 12, 2024, food inflation has still remained at an elevated level of 8.69% in May 2024 as compared to 8.70% in April 2024. The rise in food inflation was led by an increase in the inflation rate of vegetables (27.33%) followed by pulses and products (17.34%), cereals and products (8.69%) among others. Factors such as intense heatwaves, vagaries of monsoon, crop damage, uncertainty in the international commodity prices may aggravate the food inflation situation going ahead.

In this context, it is important to note that the adoption of easy and accommodative monetary or fiscal policies has the potential to generate aggregate demand and accelerate economic growth. However, the threat of inflation looms large if there is no commensurate increase in the aggregate supply in the economy which is necessary to maintain the equilibrium. This is particularly significant as the economy is experiencing a dwindling growth in the agriculture sector. Moreover, the results of May 2024 round of bi-monthly households’ inflation expectations survey released by the RBI on June 07, 2024 reveal that the inflation is expected to increase by 20 bps and 10 bps in upcoming three months and one year respectively.

As per the official estimates of GoI, India has ensured a decent economic growth where it is estimated to achieve 8.2% growth rate in 2023-24 in real terms amidst several impediments. The RBI has also been able to ensure the ‘disinflation glide path’ while taming the headline inflation. However, it is also important to note that the RBI has not yet achieved the mandated inflation target of 4.0% adopted in the flexible inflation targeting framework on a sustainable basis. Keeping all these factors in mind, in the upcoming monetary policy resolutions, the monetary policy committee of RBI should be focussing on achieving the price stability in the economy on a durable basis before arriving at any rate cuts.